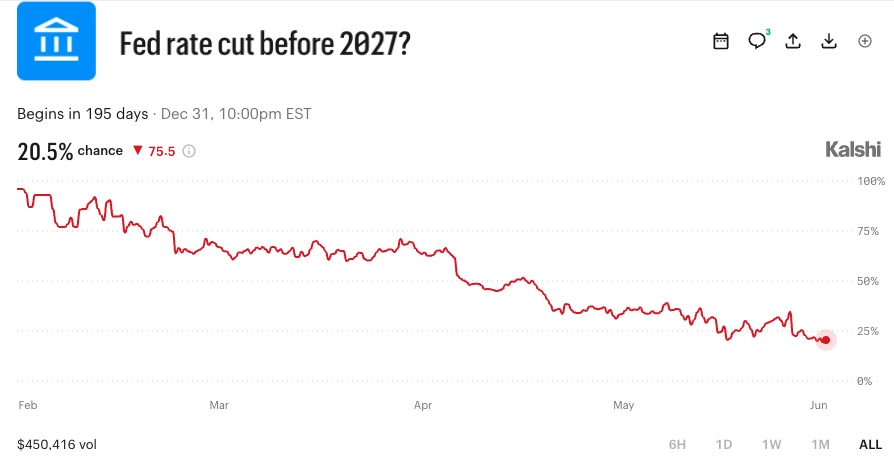

For those unaware, economic indicators, including the Fed interest rate, are a major contract in prediction markets. Some traders are pure speculators, but more and more are institutional investors using prediction markets as hedges against interest-rate changes and collateral impacts on their portfolios.

Traders on major prediction platforms moved quickly after the Federal Open Market Committee held rates steady but delivered firmer projections under new Chair Kevin Warsh. The June 16-17 Fed meeting kept the federal funds target range at 3.50% to 3.75%, but updated dot plots and messaging reduced easing expectations while lifting tightening odds for later in 2026.

This shift triggered immediate repricing as traders digested the committee’s data-dependent stance and removal of prior easing language. Timing in these markets is key to capturing temporary edges between public information releases and contract price adjustments.

Prediction Platforms Capture Rapid Shift in 2026, Tightening Odds

Kalshi traders raised the probability of a rate hike sometime in 2026 from 35% before the meeting to 57% afterward. Related contracts showed 72% odds of at least one hike before July 2027. Polymarket similarly moved to approximately 67% for a 2026 hike, with the main contract surpassing $2.5 million in volume.

Pre- and Post-Meeting Shifts in Key Rate Hike Probabilities

| Platform / Contract | Pre-Meeting Probability | Post-Meeting Probability |

|---|---|---|

| Kalshi – Fed Hike in 2026 | 35% | 57% |

| Polymarket – Fed Hike in 2026 | 28-35% | 67% |

| Kalshi – Hike Before July 2027 | Not specified | 72% |

Even though the near-term hold matched expectations, traders zeroed in on the longer horizon and hawkish tilt.

Dot Plot and Statement Changes Drive Reassessment

The Summary of Economic Projections lifted the median federal funds rate forecast for end-2026 to 3.8%. Nine of 18 officials projected at least one 25-basis-point hike by year-end. The policy statement dropped previous hints of easing while keeping the current rate decision unchanged.

Warsh emphasized ongoing work on price stability, described labor markets as stable, and highlighted favorable productivity trends. He announced task forces on communications, the balance sheet, data sources, productivity, jobs, and inflation dynamics, stressing reliance on incoming data over market reactions.

Traders Position for Data-Dependent Path Ahead

Contracts on specific meeting outcomes and year-end levels saw heightened activity. Traders are turning to July CPI, employment reports, and future projections for clearer signals on whether inflation pressures will ease or persist.

Warsh’s direct tone during his first press conference, with reduced forward guidance, reinforced the cautious approach. As new data arrive, contract prices continue to adjust in real time, often moving ahead of traditional futures and surveys.

The repricing extended to longer-dated contracts, sustaining elevated odds of tightening through 2027 and 2028. This gives traders multiple avenues for contracts to express views on timing and magnitude and to diversify and hedge their trading portfolios.

Warsh’s task-force plans hint at potential evolution in how the Fed gathers information and communicates. Overall, the June meeting showed how swiftly traders incorporate new policy signals. The combination of steady rates today with firmer projections for tomorrow produced a clear directional shift across platforms and traditional markets alike.