If you’ve spent any time trading on Polymarket or Kalshi, you already know the pitch: prediction markets are supposed to be efficient, crowd-sourced probability machines. Most of the time, they are. But “most of the time” is doing a lot of work in that sentence — and the gaps are where the money is made.

This post walks through the exact process I use to find markets where the listed price and the real probability have drifted apart. It’s not a magic formula, and it won’t turn you into a full-time quant overnight. But it is a checklist you can start applying to your own trading today.

Why This Matters: What “Mispriced” Actually Means

Before hunting for an edge, it helps to define the target. A market is “mispriced” when the implied probability (the price of a YES share, roughly) diverges meaningfully from the true probability of the event — not because you have a hot take, but because you can point to a concrete, verifiable reason the crowd hasn’t priced it in yet.

That distinction matters. Thinking that a market is wrong because you feel differently isn’t an edge. Edge comes from information, math, or structural factors that the current price hasn’t absorbed.

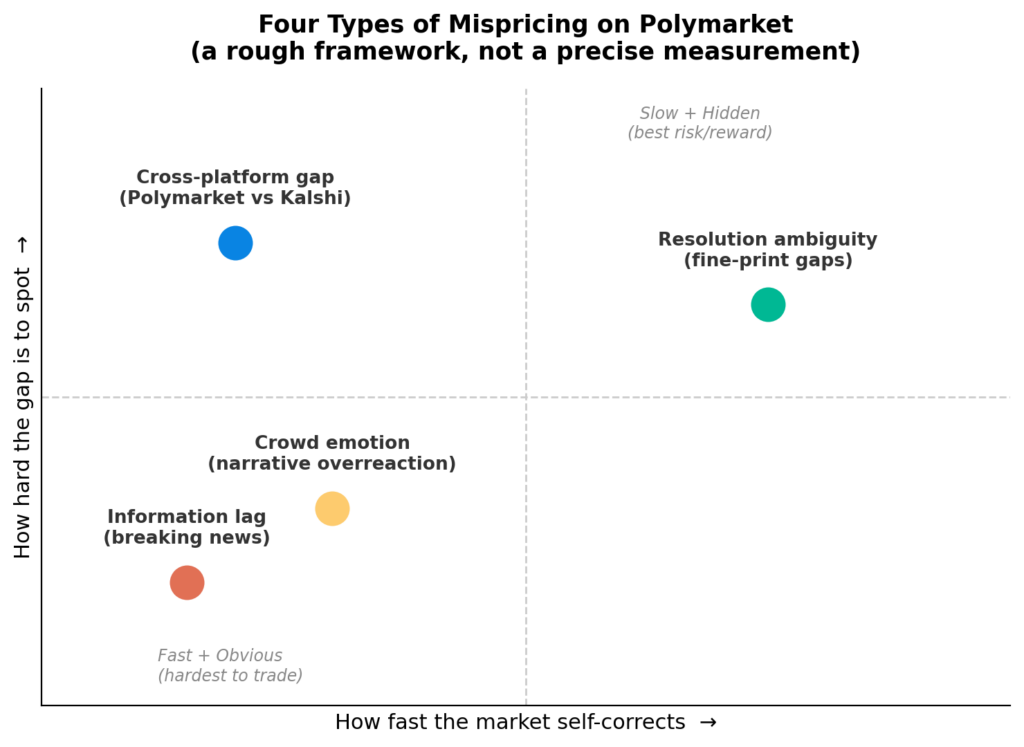

What Causes Prediction Markets to Get Mispriced

Mispricing on platforms like Polymarket and Kalshi tends to come from a handful of repeatable sources. Understanding these is more valuable than any single trade, because they’re the patterns you’ll keep seeing over and over.

| Cause | Why It Happens | Where You’ll Spot It |

| Thin liquidity | Few traders means wide spreads and stale prices | Niche politics, local sports, small-cap crypto markets |

| Information lag | News breaks faster than the market repriced | Breaking political or corporate news events |

| Behavioral bias | Traders overweight vivid, recent, or popular outcomes | Longshot “moonshot” markets, celebrity-driven markets |

| Resolution ambiguity | Traders misjudge how a market will actually settle | Markets with vague or technical resolution criteria |

| Herding / narrative momentum | Price moves with the crowd’s mood, not new data | High-volume political and entertainment markets |

| Cross-platform gaps | The same event is priced differently on two platforms | Same election/sports outcome on Polymarket vs. Kalshi |

Each of these gives you a different way of finding an opening. The rest of this post breaks down how I actually go looking for them.

Step 1: Build an Estimate Before You Look at the Price

This is the step almost everyone skips, and it’s the one that separates disciplined edge-finding from gut-feel gambling.

Before I check what a market is trading at, I try to write down my own probability estimate using:

- Base rates. How often has this type of event happened historically? (Incumbent re-election rates, average time-to-resolution for legal cases, historical odds of a Fed rate move given similar economic data.)

- Public forecasting sources. Polling aggregators, expert forecasts, sportsbook lines (useful as a sanity check even if you don’t bet there), and academic or institutional models.

- First-hand information. Anything you know from direct research — earnings reports, court filings, regulatory filings, primary sources — that hasn’t been widely discussed yet.

Only after I have a number do I go check the market price. This order matters. If you look at the price first, you’ll unconsciously anchor to it, and every “edge” you think you find will really just be you rationalizing the crowd’s number.

Step 2: Where to Actually Look for Mispriced Markets

Not all corners of a prediction market platform are equally likely to hide edge. I focus my scanning time on a short list of categories:

- Low-volume, low-liquidity markets. Wide bid-ask spreads and thin order books mean the “crowd” pricing the market might really be a handful of traders. These are the highest-variance but highest-edge opportunities if you have real information.

- Markets that haven’t moved after relevant news. A market sitting flat for hours after a related headline drops is a strong signal that either nobody’s noticed, or nobody’s bothered to trade it yet.

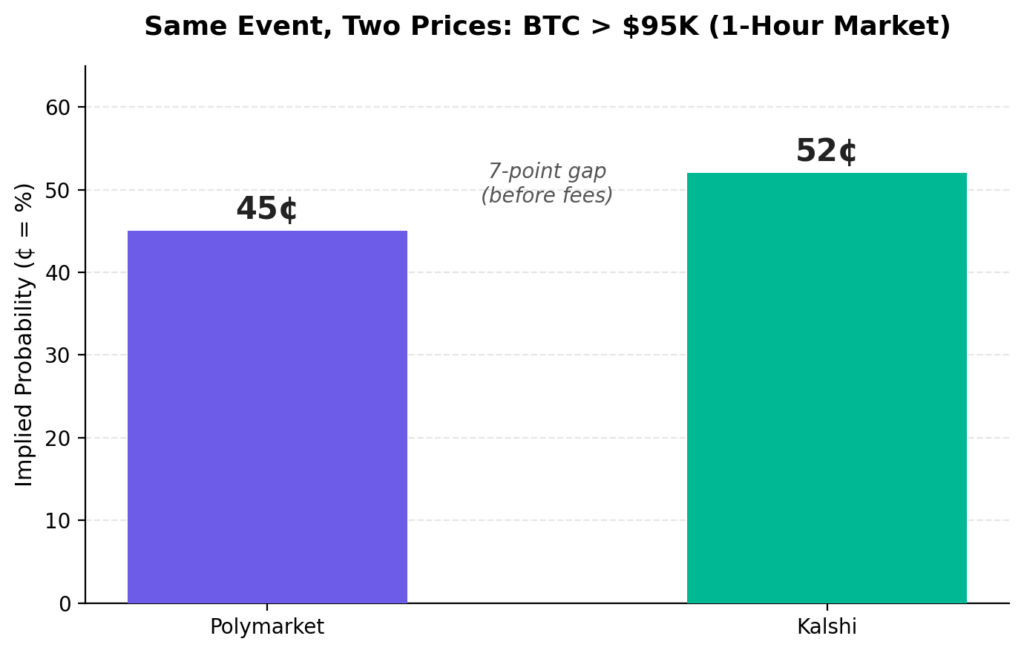

- Cross-platform duplicates. When the same real-world event has contracts on both Polymarket and Kalshi, compare the implied probabilities directly. A meaningful gap, after accounting for fees, is close to risk-free edge if you can trade both sides.

- Markets with tricky resolution criteria. Read the actual resolution rules, not just the market title. Traders often price the headline question rather than the fine print — and the fine print is where mispricing hides.

- Recently launched niche markets. New market categories (weather, niche entertainment, obscure legal outcomes) often launch before enough informed traders show up to correct early pricing errors.

Step 3: Compare Your Estimate to the Market Price

Once I have my independent estimate and the current market price, I look at the size of the gap and ask three questions:

- Is the gap bigger than my own margin of error? If my estimate has a wide error bar (say, plus or minus 10 points), a 3-point gap isn’t edge — it’s noise.

- Can I explain why the market hasn’t corrected yet? If I can’t point to a liquidity, attention, or information reason, I should be suspicious that the market actually knows something I don’t.

- Does the gap survive fees and spread? On some platforms, fees and the bid-ask spread alone can eat a 2-3 point “edge” before you’ve made a single trade.

If a market clears all three checks, it goes on my shortlist.

Step 4: Size the Position Based on Confidence, Not Conviction

Finding a mispriced market is only half the job — sizing the trade correctly is what actually protects your account over time. A few rules I follow:

- Never bet as if your estimate is certain. Your “true probability” is itself an estimate with error. Position size should reflect your confidence in that estimate, not just the size of the perceived gap.

- Use a fraction of a formal sizing method (like Kelly), not the full amount. Fractional Kelly sizing accounts for the fact that your edge estimate could be wrong.

- Cap exposure to any single event or theme. Correlated markets (multiple contracts tied to the same election or the same court case) can wipe out a portfolio all at once if you’re not tracking correlation.

What This Looks Like in Practice

It helps to walk through the pattern in the abstract, since actual trade details and prices change by the day and shouldn’t be treated as a template to copy blindly.

Pattern 1 — The stale market after news. A regulatory or legal market sits at roughly the same price for several days. Then a filing or court ruling drops that clearly shifts the odds of the underlying outcome. If the market hasn’t moved within an hour or two of that news being public, it’s worth checking the resolution criteria to confirm the news is actually relevant to how the market resolves — not just the general topic — before trading it.

Pattern 2 — The illiquid niche market. A newly listed market in an obscure category (a regional election, a niche sports outcome, a specific corporate decision) has almost no volume. The listed price reflects the last trade from a single participant, not a broad consensus. If you can build a solid base-rate estimate here, the “market” you’re really trading against is one or two people, not the wisdom of a crowd.

Pattern 3 — The resolution-criteria trap working in your favor. Sometimes the crowd prices the headline question, but the actual contract resolves on a narrower technical definition. When the technical definition is easier to satisfy than the headline suggests, the market can be underpriced relative to its real resolution odds — and vice versa when it’s harder to satisfy.

In every case, the common thread isn’t a secret data source. It’s the discipline of asking, “What specifically is this contract measuring, and has the price actually caught up to what’s publicly known about it?”

Tools and Habits That Make This Repeatable

You don’t need an expensive terminal to run this process consistently. A few low-cost habits do most of the heavy lifting:

- A running spreadsheet of your estimates. Log the market, your pre-trade probability estimate, the market price at entry, your reasoning for the gap, and the eventual outcome. This is what lets you check your own calibration honestly later.

- Alerts on relevant news sources. For any market you’re tracking, set up a simple alert (Google Alerts, RSS, or a news aggregator) for the underlying event so you’re not relying on manually refreshing a market page all day.

- A standing base-rate reference. Keep a simple reference document of historical base rates for event types you trade often (incumbent win rates, average legal case durations, historical volatility bands for the assets you follow). Building this once saves you from re-deriving it under time pressure every time a market catches your eye.

- A short pre-trade checklist. The six-question checklist below, run every time, before you place a trade — not just when a market “feels” obviously wrong.

A Simple Mispricing Checklist

Here’s the condensed version I actually run through before placing a trade:

| Check | Question |

| Independent estimate | Did I form a probability before looking at the market price? |

| Explainable gap | Can I name the specific reason (liquidity, lag, bias, ambiguity) the market hasn’t corrected? |

| Error margin | Is the gap bigger than my own uncertainty in the estimate? |

| Fees and spread | Does the edge survive after transaction costs? |

| Correlation | Am I already exposed to this event through other positions? |

| Resolution risk | Have I read the exact resolution criteria, not just the title? |

If a market fails more than one of these, I pass — no matter how tempting the headline number looks.

Common Mistakes That Look Like Edge (But Aren’t)

- Confusing “different opinion” with “mispricing.” Disagreeing with the market isn’t the same as having information the market lacks.

- Ignoring resolution risk. A market can look mispriced right up until it resolves in a way you

- didn’t expect because you skipped the fine print.

- Underestimating fees on thin markets. Wide spreads on illiquid markets can quietly erase most of an apparent edge.

- Overconfidence after a few wins. A handful of correct calls can feel like validation of a flawed process. Track your calibration over dozens of trades, not five.

- Chasing narrative-driven markets. The most talked-about markets (viral political or entertainment events) tend to attract the most attention and the most efficient pricing — precisely because everyone’s looking at them.

Frequently Asked Questions

Do I need to be a data scientist to do this?

No. A spreadsheet, a clear base-rate estimate, and the discipline to write your number down before checking the price will get you most of the way there.

Which platforms tend to have the most mispricing?

Newer or lower-volume categories on any platform — including Polymarket and Kalshi — tend to have wider gaps than flagship political or macro markets, simply because fewer informed traders are watching them.

Is cross-platform arbitrage still viable?

It shows up periodically, especially around major news events when one platform reprices faster than another. It tends to close quickly once spotted, so it rewards speed and platform access on both sides.

How do I know if my “edge” is real or just luck?

Track every trade with your pre-trade estimate, the market price at entry, and the outcome. Over enough trades, well-calibrated estimates should track actual outcomes closely — that consistency is the real test, not any single winning trade.

The Takeaway

Finding mispriced prediction markets isn’t about having a secret formula — it’s about consistently doing the boring parts other traders skip: forming an independent estimate first, understanding why a gap exists before trading it, and sizing positions like your estimate could be wrong, because it sometimes will be.

The edge isn’t in being smarter than the market on every single trade. It’s in being disciplined enough to only take the trades where you can actually explain the gap.

Colin is a long-time digital media channel operator and content creator with an intense interest in sports gaming, prediction markets, and artificial intelligence, and how they are shaping the social, entertainment, and economic landscapes.