A Guest Author Post from Jacob Wyngaard, an Applied Mathematics PhD student at the University of Delaware, focused on probability, market design, and prediction markets. He is launching a social gambling start-up called Prediction Wizard

A model-based look at when prediction market pricing can beat traditional sportsbook pricing.

Prediction markets are often claimed to offer sharper pricing than sportsbooks. More traders, more competition, better odds. But recent analysis from Citizens suggests that isn’t always true.

So, when should we actually expect a prediction market to offer better pricing than a sportsbook?

This article takes a simple approach: build a clean mathematical model of both systems, feed them the same set of bettors, and see which one produces the best prices.

Model Assumptions

At a high level, sportsbooks set prices, while prediction markets let prices emerge from trade. I modeled both sports book and prediction market trading on a two-outcome event under the following assumptions:

- Each bettor has a subjective probability pi for the favored outcome and a corresponding wager size bi. This follows the classical framework introduced by Eisenberg and Gale (1959) in their analysis of pari-mutuel markets.

- The sportsbook knows the underlying distribution of bettor beliefs and wager sizes.

- The sportsbook chooses prices to maximize profit subject to a balanced-book constraint. Although Levitt (2004) provides evidence that sportsbooks may deliberately accept unbalanced action, I abstracted from this behavior.

- Bettors trade only when the expected value is positive, according to their own beliefs.

Note. The model is not intended as a literal description of how all sportsbooks or prediction markets operate. It asks: if both systems face the same population of beliefs and wager sizes, what kind of price advantage should we expect prediction markets to have?

How Sportsbook Pricing Works in the Model

Sportsbook prices are represented by the usual moneyline pair: a favorite priced at −α and an underdog priced at +β. The interpretation is straightforward: α tells you how much you need to bet to win $100 on the favorite, while β tells you how much profit you earn from a $100 bet on the underdog. In closely matched games, both sides may even be listed with negative odds.

Side Line

Favorite −α

Underdog +β

These lines imply two cutoff probabilities:

α β

pα = α + 100 , pβ = β + 100 .

A bettor takes the favorite only if their belief in the favorite exceeds pα, and takes the underdog only if that belief is below pβ.

To aggregate beliefs, we define f (p) as the distribution of bettor capital across subjective probabilities, and let

be the associated cumulative distribution.

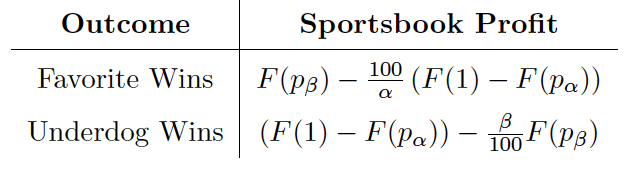

Given this structure, sportsbook profits under each outcome can be written as:

Under the assumption (c), sportsbooks choose (pα, pβ) to maximize profit while ensuring equal profit across outcomes.

This leads to a constraint function for profit balancing:

and an objective function for profit maximization:

Assuming F is continuously differentiable, we can apply the method of Lagrange multipliers to obtain the first-order condition:

The balanced-book assumption leads the sportsbook to choose (pα, pβ) to satisfy both the constraint function and this first-order condition.

How Prediction Market Pricing Works in the Model

Prediction markets work differently. Instead of setting odds directly, they match buyers and sellers. Prices emerge from a bid–ask system where:

pask − pbid ≥ 0.

As in the money-line case, traders decide whether to participate based on their expected value. Here, this expected value must also include the fees.

On Kalshi, fees for trading C event contracts for price p are of the following form:

Fee = round up(rp(1 − p)C)

where r = .0175 for market makers and r = .07 for market takers. To keep the model tractable, I approximated Kalshi’s discrete fee schedule with its continuous counterpart.

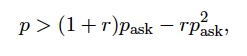

A trader buys only when the expected value under their belief is positive:

and sells only when:

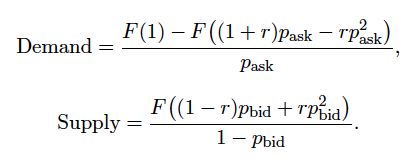

Aggregating those decisions produces model-based demand and supply functions:

The market-clearing bid and ask prices are the ones for which supply equals demand.

Testing the Systems

To compare the two systems, I parameterized bettor beliefs using a Beta distribution with mean µ

and standard deviation σ, over the grid

µ ∈ {0.05, 0.06, . . . , 0.95}, σ ∈ {0.01, 0.02, . . . , 0.07}.

I furthermore parameterized the prediction market bid-ask spread over the grid

pask − pbid ∈ {0, 0.01, . . . , .08},

For each pair (µ, σ) and prediction market bid-ask spread pask − pbid,

- I solved for the sportsbook pα and pβ value candidates using a multi-start bounded non-linear least-squares method and selected admissible solutions,

- I solved for the prediction-market equilibrium prices using Brent’s method as a primary solver with bounded minimization as a fallback,

- I compared sportsbook odds to the prediction market fee-adjusted effective buy and sell thresholds.

When calculating fees, I assumed the market taker rate r = .07 The key condition for checking was:

pβ ≤ pbid − Fee and pask + Fee ≤ pα.

If that held, then the prediction market price was at least as high as the sportsbook’s for that parameterization.

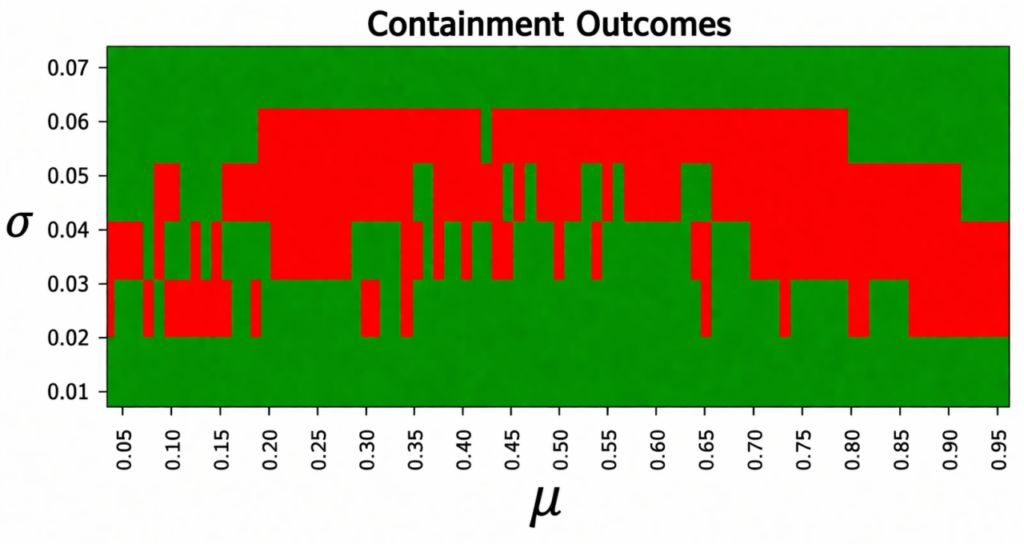

Results

Here’s the key question: when does the prediction market actually beat the sportsbook? The heatmap below answers that across the full (µ, σ) grid for pask − pbid = .05.

Note. Green regions are the parameter combinations where prediction markets beat sportsbooks on price in this model. Red regions are where that advantage disappears.

Two patterns stand out. Prediction markets tend to outperform sportsbooks when beliefs are either highly concentrated or strongly dispersed, whereas sportsbooks are more competitive in intermediate regions. This may help explain why the Citizens analysis found sportsbook pricing to be more competitive.

However, as the prediction market spread decreases, the region of prediction market pricing dominance expands. This spread is reported in the table below, which reports the percentage of valid parameter pairs for which prediction market pricing beats sportsbook pricing.

| PAsk − PBid | Percent of Parameter Values for which Prediction Markets have Better Prices (%) |

| 0% | 99.37 |

| 1% | 97.96 |

| 2% | 92.62 |

| 3% | 84.30 |

| 4% | 74.73 |

| 5% | 68.13 |

| 6% | 56.67 |

| 7% | 37.99 |

| 8% | 27.79 |

The decline is steep. With minimal bid-ask spread, prediction markets dominate in almost all valid cases. With a spread of 8%, prediction markets offer better pricing in less than 28% of cases.

Bottom Line

Within this model, prediction markets can offer better pricing when liquidity keeps bid-ask spreads tight. Modest increases in spread that do occur sharply reduce the frequency with which prediction markets offer better pricing.

So the practical takeaway is not that prediction markets always have better fee-adjusted effective pricing for bettors. It is that they do so most reliably when liquidity is good enough to keep spreads tight.

Final Caveat

This is a model-based exercise, not a universal empirical claim. The conclusions depend on:

- The assumed distribution of bettor beliefs,

- The equilibrium concept is used on both sides,

- The way the fees are imposed.

Still, the exercise gives a useful benchmark. Under this model, prediction markets in high liquidity markets frequently generate better pricing than sportsbooks.

Jacob Wyngaard is an Applied Mathematics PhD student at the University of Delaware, focused on probability, market design, and prediction markets. He is launching a social gambling start-up called Prediction Wizard